GSTR-3B filing mistakes 2026 have become one of the biggest reasons why GST notices are increasing across India. With the GST system now heavily automated and closely monitored, even small errors in GSTR-3B can trigger notices, interest demands, or ITC reversals.

Filing GSTR-3B in 2026 is no longer a routine monthly task—it has become a high-risk compliance activity due to real-time data matching between GSTR-1, GSTR-3B, GSTR-2B, and the e-Way Bill system.

Why GSTR-3B Scrutiny Is Higher in 2026

The GST ecosystem is increasingly driven by technology and analytics managed by GSTN under policy supervision of CBIC.

Key changes impacting taxpayers:

Auto-locking of outward supply values

Strict ITC validation through GSTR-2B

Integration with e-Way Bill data

System-generated notices without manual intervention

In short, manual errors now have automatic consequences.

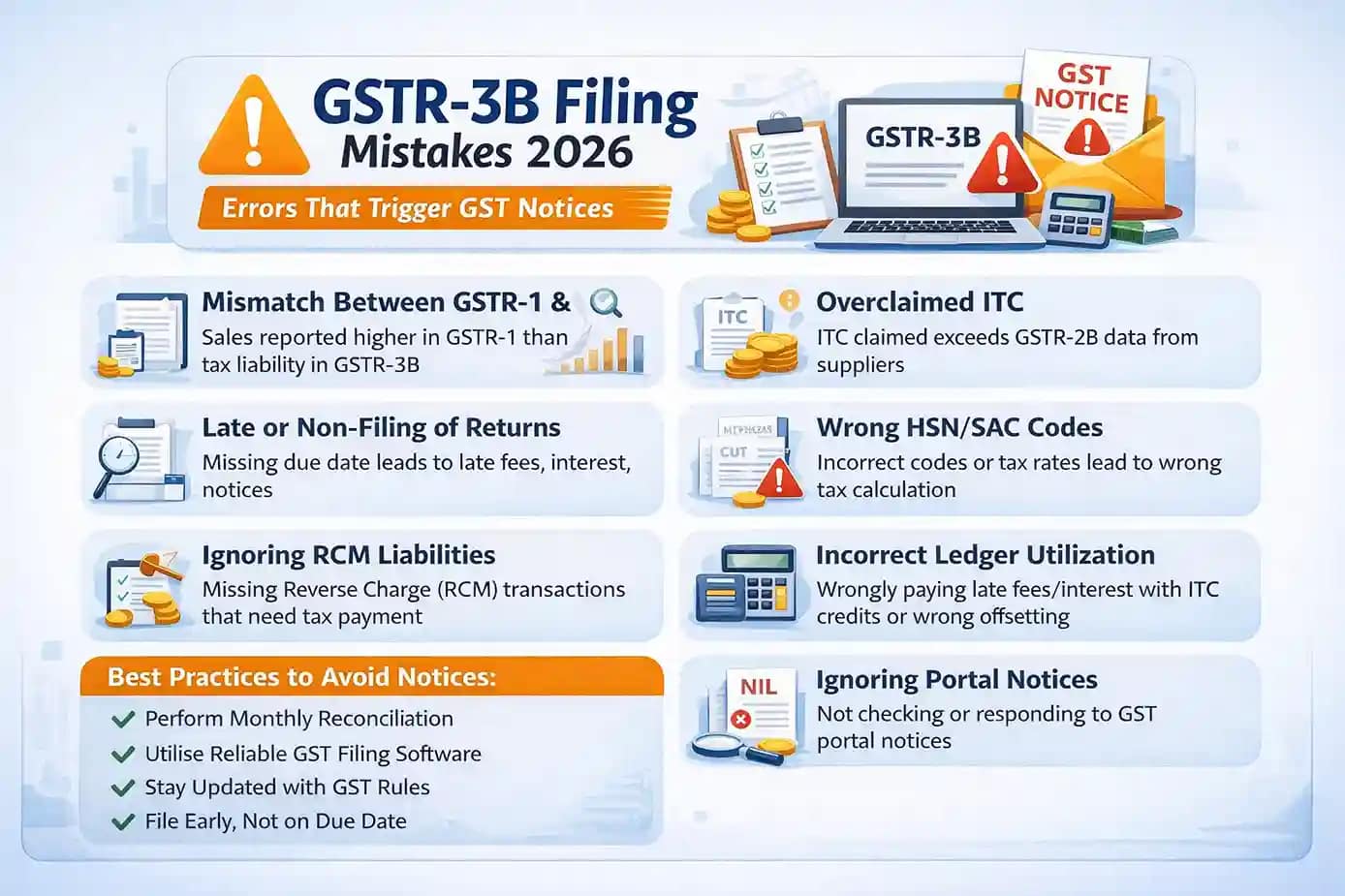

1. Mismatches and Data Discrepancies (Biggest Notice Trigger)

GSTR-1 vs GSTR-3B Mismatch

Reporting higher sales in GSTR-1 than the tax liability declared in GSTR-3B is one of the most common red flags.

From recent updates:

Outward supply figures in GSTR-3B are increasingly aligned with GSTR-1

Corrections must be made first in GSTR-1

Post-filing explanations are rarely accepted without payment

Result: Notice under Rule 88C / DRC-01C

GSTR-2B vs ITC Claimed in GSTR-3B

Claiming ITC that does not appear in GSTR-2B is now automatically detected.

Common causes:

Supplier has not filed GSTR-1

Invoice uploaded late by supplier

Ineligible ITC claimed by mistake

Result: Notice under Rule 88D with interest and reversal demand

e-Way Bill vs Return Data Mismatch

When goods movement data (quantity/value) in e-Way Bills does not match reported turnover, it raises suspicion of under-reporting.

Table : Common Data Mismatch Errors

| Area of Mismatch | What Goes Wrong | Likely Consequence |

|---|---|---|

| GSTR-1 vs GSTR-3B | Higher sales in GSTR-1 | Rule 88C notice |

| GSTR-2B vs ITC | Excess ITC claimed | Rule 88D notice |

| e-Way Bill data | Turnover mismatch | Department scrutiny |

| Amendments delayed | Late corrections | Interest + penalty |

2. Incorrect HSN/SAC Codes and Tax Rates

Using the wrong HSN or SAC code, or applying an incorrect GST rate, is treated seriously in 2026 due to automated classification checks.

Examples:

Treating inter-state supply as intra-state

Applying lower GST rate to taxable goods

Incorrect service classification

Impact: Demand for differential tax, interest, and possible penalty for misreporting.

3. Operational and Compliance Errors That Invite Notices

Late or Non-Filing of GSTR-3B

Late filing attracts:

₹50 per day late fee (₹20 for Nil return)

18% annual interest on tax due

Blocking of e-Way Bill generation

Risk of GST registration suspension

Not Filing Nil Returns

Even if there are no transactions, a Nil GSTR-3B must be filed.

Many taxpayers wrongly assume “no business = no return,” which leads to system-generated late fees.

Understanding GSTR-3B Filing Mistakes is essential in 2026 because the GST system now relies on automated data matching across multiple returns.

Ignoring Reverse Charge Mechanism (RCM)

RCM liabilities are often missed on:

Legal services

Transport services

Certain unregistered supplier transactions

Result: Short payment of tax + interest + penalty.

Incorrect Ledger Utilisation

Common mistakes include:

Paying interest or late fee using ITC (not allowed)

Wrong utilisation order of CGST/SGST/IGST

Incorrect cash vs credit offset

Table : Compliance Errors and Their Impact

| Error Type | Common Mistake | Consequence |

|---|---|---|

| Late filing | Missing due date | Late fee + interest |

| Nil return ignored | No filing done | Auto late fee |

| RCM missed | Tax not paid | Demand + penalty |

| Ledger misuse | Wrong offset | Payment mismatch notice |

| Portal alerts ignored | Notices missed | Ex-parte orders |

Ignoring Notices on the GST Portal

All official communications are uploaded on the GST portal dashboard. Missing or ignoring them can lead to:

Ex-parte assessment orders

Automatic recovery proceedings

Blocking of refunds and ITC

Best practice: Check the GST portal at least once a week, even after filing returns.

Also Read:-https://gstandtax.com/gst-due-dates-2026-2027/

Best Practices to Stay Notice-Free in 2026

Monthly Reconciliation (Non-Negotiable)

Always reconcile:

GSTR-1 vs GSTR-3B

GSTR-2B vs ITC claimed

Books of accounts vs returns

Use Software & Automation

Reliable GST software helps:

Auto-validate HSN/SAC codes

Detect mismatches before filing

Reduce manual entry errors

Stay Updated with GST Changes

GST rules and portal features change frequently. Follow updates issued by GSTN and CBIC to remain compliant.

File Early, Not on Due Date

Last-minute filing increases the risk of:

Portal downtime

Missed errors

Panic corrections

Final Thoughts

In 2026, GST notices are no longer random—they are system-driven. Most notices arise not due to fraud, but because of small, avoidable compliance mistakes.

A disciplined approach to reconciliation, timely filing, and regular portal monitoring can keep your business compliant, stress-free, and notice-free.

By identifying and correcting GSTR-3B Filing Mistakes on time, taxpayers can avoid GST notices, interest, and unnecessary penalties.

2 thoughts on “GSTR-3B Filing Mistakes That Trigger GST Notices in 2026 – Avoid These Costly Errors”